Illustration by Anna Roth

Financial Responsibility

Managing your own finances and learning how to effectively spend and save is an important part of becoming an adult, for people both with and without disabilities. Whether your goal is to save money for education or housing or to reduce debt, the key is developing a budget. Each person’s budget will depend on their specific circumstances, but certain basics apply to all, and effective planning is the first step.

Budget Planning

A budget is a plan, and the first step in creating one is to ask yourself key questions, including:

- What are my goals? Examples might include saving for education, housing, transportation, vacation, retirement, etc.

- How much time do I want to give myself to achieve these goals? For instance, some may be short-term, achievable in week or months, while others may take years to reach.

- Will I be receiving any financial assistance? Examples might include scholarships, grants, family assistance, government benefits, etc.

- Will someone else have access to my financial accounts? Examples might include a co-signer on a loan, joint checking account holders or an authorized user on a credit card.

- What is my credit score? (See below for more information on credit and credit scores.)

Once you’ve answered these key questions, even if in general terms, you can start developing your budget. This starts with examining your income. If you work, it is important to understand that your salary (gross income) and your take home pay (net income) will be different. Your paycheck will also have deductions. These deductions include federal income tax and contributions under the Federal Insurance Contributions Act (FICA).FICA contributions are 6.2% of your gross wages for Social Security and 1.45% for Medicare. Your employer matches these percentages. Federal income taxes will start at an average 10% and gradually increase along with your income.

Depending on your employer and employment situation, you may also have the option of enrolling in employer sponsored benefits such as health care plans, dental plans and retirement plans. These benefits may be removed before or after taxes are deducted, depending on different circumstances.

If you earn over a certain amount, you will also need to file income taxes annually. There are various resources available to help you do this, such as the Internal Revenue Service’s (IRS) Volunteer Income Tax Assistance program (VITA); local university, college or community clinics; and free online software.

Preparing a budget starts with examining income. Consider this example:

Jim works full time (40 hours weekly) in a store. He earns $10 an hour and is paid bi-weekly (every 2 weeks). He is enrolled in his company’s health care plan, and his share of the premiums is $50 bi-weekly. Per the calculation below, this translates to a bi-weekly take home pay (net income) of $660.00.

You should keep in mind, when examining income, that earned income can affect some Social Security benefits.

Once you know your take home pay (net income) you can calculate your expenses to budget accordingly. When developing a budget, the following are some factors to consider, but there may be others depending on your specific circumstances.

- Housing – Housing costs are usually monthly rent or, if you own your own home, a mortgage payment. They are impacted by many factors. For young people, one of these is whether you live with parents/guardians, on your own or with roommates.

- Bills and Utilities – These may include electricity, water, gas, internet and phone. Some of these expenses may be included in rent, while others may not.

- Transportation – Transportation costs may include a car loan payment, car insurance premium, gas, bus passes, ride share services, etc.

- Food – Groceries, snacks, meal plans, restaurant/takeout expenses, etc.

- Other Expenses – These may include things like

tuition, health insurance (if not obtained through

your employment) homeowner’s or renter’s insurance, pets, hobbies, recreation, car or home maintenance, travel, etc.

|

Gross Income |

$800.00 |

($10 x 40 hours per week x 2 weeks) |

|

|

Benefits Deduction |

-$50.00 |

($50 for health care) |

|

|

Tax Deductions |

-$90.00 |

-12% |

|

|

Net Bi-weekly Income |

$660.00 |

|

|

Establishing Good Credit

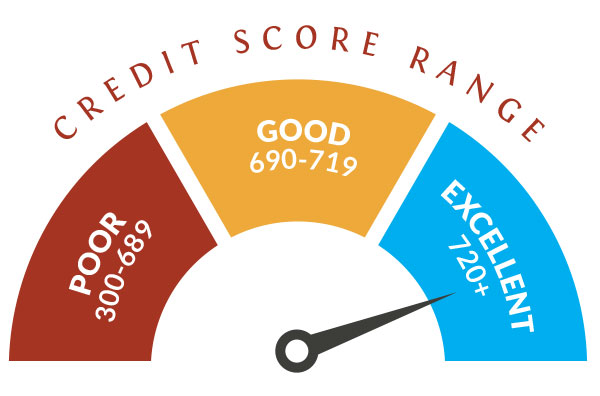

A credit score is a number that indicates how likely you are to pay back a loan. Banks and other potential lenders consider your credit score when deciding whether to loan you money, for instance, to purchase a car or your own home. Your credit score is determined on your credit history, which includes your current accounts and level of debt, previous loan history, and other factors. The higher your credit score, the better you look to potential lenders as creditworthy.

Generally, credit scores range from 300-850. A good credit score falls between 690-719 and an excellent credit score is 720 and above. Again, many factors affect your credit score, and the score can move up and down. Every time you apply for a new credit card or loan, your credit score is checked. Potential landlords and housing associations may also run credit checks.

As a result, it is important you know and keep track of all minimum payments required for any debt you currently have. As a general rule, having debt does not hurt your credit score; rather, not making required payments on time does. Factors that lower your credit score include late or missing payments, having too many credit inquires in a short period of time, carrying high balances in comparison to available credit, length of credit history and defaulting on a loan.

Many financial institutions will allow you to access your credit score without affecting your credit score. Reviewing your credit and financial statements to identify discrepancies is also important because identity theft has become a growing concern. If you are concerned about identity theft, there are options available to help, such as enrolling in your bank or credit card company’s credit protection program or having a temporary credit freeze that restricts access to your credit file.

In Florida, child welfare agencies are able to obtain credit reports from children starting at age 14, provide them to the individual and help them deal with issues.

Tips and Resources

The following steps can assist in establishing a solid financial foundation and building good credit:

- Enroll in a personal finance course.

- Use your bank’s online resource guides.

- Before opening a new bank account, make sure you have all required information and documents; different banks may have different requirements.

- Use a phone app to track your saving and spending.

- Be aware of websites that will unnecessarily run your credit and charge you to find out your score.

For youth with disabilities who receive Supplemental Security Income (SSI), additional considerations may come into play when budgeting and financial planning. For more information, see the next section of this guide.